The Best Health Insurance for Dental Clinics: A Practical Guide for Dentists

Sorting out health insurance for your dental clinic? You’re not alone. Dentists spend years learning about crowns and root canals and not health insurance jargon for their business. But your practice (and your people) depend on health benefits coverage.

Let’s make it simple—and maybe a little less painful.

Why Health Insurance Matters for Dental Clinics

If you own or manage a dental practice, you know how competitive hiring is. Hygienists, dental assistants, and office staff are in demand. Offering great health, dental, and vision coverage isn’t just a perk—it’s your edge in attracting top talent and keeping your star employees from leaving.

In fact, 88% of workers rank health benefits as one of the most important parts of a job offer. For dental practices, providing coverage also shows patients you value your team’s well-being.

The challenge? Finding a health insurance option that’s affordable and not a paperwork nightmare.

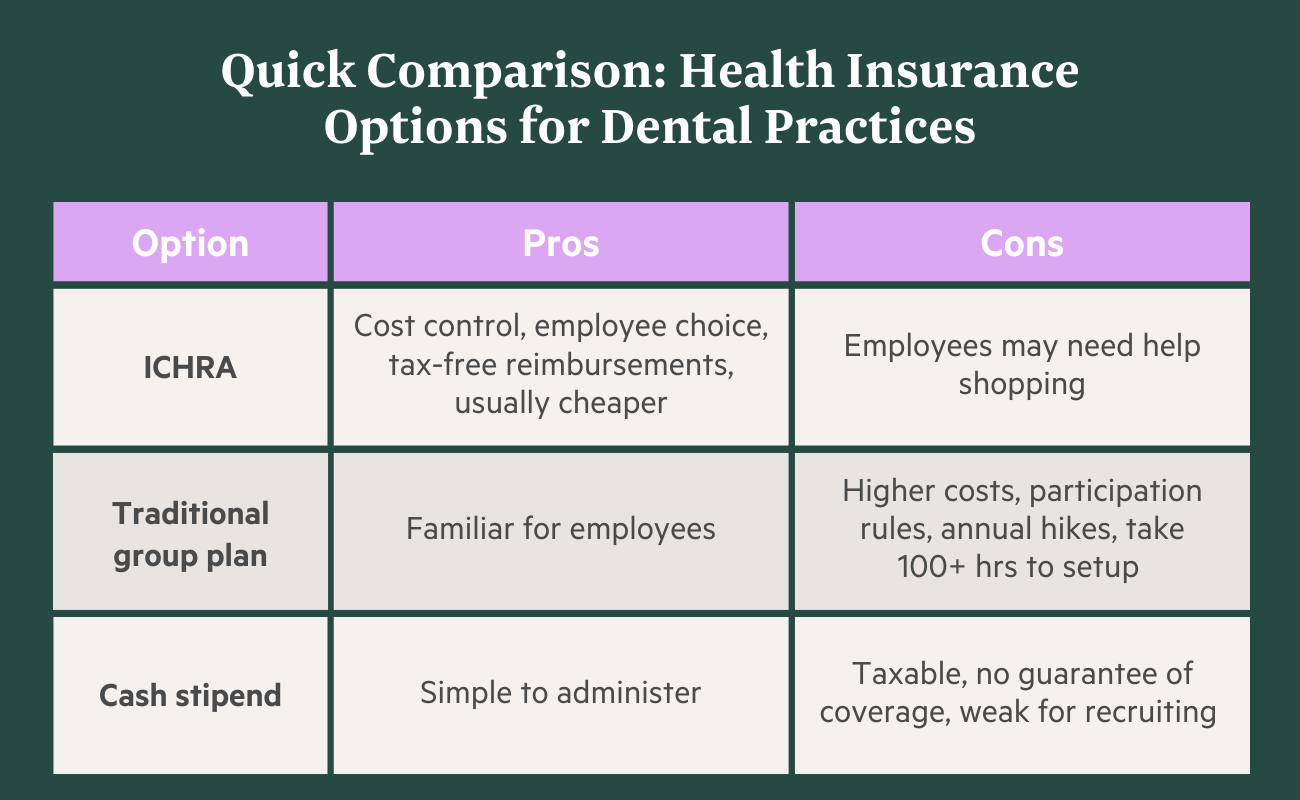

Health Insurance Options for Dental Clinics

When it comes to covering your team, dentist offices typically have three options. (Of course, not doing anything is an option too, but we’ll assume the reason you’re researching is to avoid that one.)

- -NEW- Individual Coverage Health Reimbursement Arrangement (ICHRA)

- Traditional Small Group Health Insurance Plan

- Cash Stipends or Wage Bumps Instead of Benefits

Each comes with pros and cons. Let’s break them down.

What is ICHRA? Why Haven’t I Heard of it?

In a nutshell, ICHRA was introduced by federal rule in 2020, and completely changed the benefits game for small business owners. For the first time, ICHRA let employers like independent dental offices provide pre-tax money to employees, which they can use to pay for the health insurance plan that fits their needs. ICHRA was introduced to give more options to businesses who were struggling to keep up with the complexity and cost of traditional small group plans.

1. ICHRA: The Flexible Favorite

Best for: Small-to-mid-sized dental clinics looking for cost control and flexibility.

How it works:

As the clinic owner, you set a pre-tax budget or “allowance”. Each staff member shops for their own health insurance (vision and dental, too) that works for them through the ACA marketplace. Your team then gets reimbursed for their premiums using your pre-tax allowance.

Why dental clinics love it:

- Cost Control: You decide your monthly spend (hard not to love this advantage).

- Team Choice: Each employee picks what fits them—a plan that includes their doctors and their medicines.

- Administrative Simplicity: The right ICHRA provider (for obvious reasons we’re biased toward StretchDollar) can get you set up in less time than it takes to order that specialty coffee.

- Often Cheaper Plans of Similar Quality: In most major metros, individual plans are cheaper than similar small group plans and sometimes by up to 20%!

What to watch for:

- Shopping Guidance Needed: For some employees, the first time navigating health insurance can feel a bit overwhelming. Consider finding an ICHRA administrator who helps your team through it. (Hint: StretchDollar offers in-house health insurance guides.)

2. Traditional Small Group Health Insurance Plans

Best for: Practices that want a familiar, “one-size-fits-all” approach.

How it works:

You (the employer) choose a plan—or a couple—for everyone.You cover at least 40% of the monthly premium, while your employees are responsible for the rest. This is the most traditional route that small businesses have accessed health insurance coverage for employees. Up until recently, traditional groups plans were considered a cheaper option than individuals shopping for their own insurance. But times have changed.

Why dental clinics often choose this:

- Familiar approach: This is the way most small businesses provide coverage, so why do something different (even if it's not ideal).

What to watch for:

- Higher Costs: Group plans typically cost more than individual plans—sometimes by 20% or more.

- Minimum Participation: Most insurers require at least 50% of eligible staff to join, which can be tough for small clinics who may have several employees on a spouse plan.

- Unpredictable Price Hikes. Renewal time is a little like gambling – you know the cost will go up, but you have no idea how much

- Heavy Admin Work: Research, renewals, and back-and-forth with brokers eat up valuable time.

- Underwriting: For some plans, your employees’ past claims and health status will matter (translation: you have to ask your employees to take a health quiz)

3. Cash Stipends or Wage Bumps

Best for: Dental clinics wanting the simplest—but least effective—approach.

How it works:

You just add cash to paychecks and hope your team finds their own coverage.

Why it sounds tempting: It’s simple. No insurance contracts, no setup.

But here’s the reality:

- It’s Taxable. Payroll taxes apply, so staff may see less than intended. And taxes are 35% or more.

- No Guarantees. No way to ensure employees buy coverage (some may skip it entirely), then what’s the boost for?

- Missed Value. Employees may not realize the “extra” is supposed to help with health insurance.

- It Doesn’t Help for Recruiting. Health insurance is the most desired benefit—cash alone won’t help you stand out.

How to Choose the Right Plan for Your Dental Clinic

When deciding, ask:

- Do I want predictable costs each month? (→ ICHRA)

- Do I prefer to stick with what’s familiar? (→ Group Plan)

- Am I okay with lower recruiting power? (→ Stipend)

If your priority is attracting and keeping great staff while keeping costs under control, ICHRA is often the best choice.

FAQs: Health Insurance for Dental Clinics

What’s the best health insurance for dental clinic employees?

For most small sized practices with under 20 employees, ICHRA offers the best balance of affordability, flexibility, and recruiting power.

How much does health insurance cost for a dental practice?

On average, individual health insurance costs around $8,900 per employee annually. Costs however will vary depending on where your employees live, their age and if they have any dependents.

Can dental clinics use ICHRA?

Yes! Any size dental clinic can set up an ICHRA—there are no participation minimums.

Do employees like ICHRA?

Yes, because it lets them choose a plan that covers their preferred doctors and prescriptions, instead of being locked into one clinic-wide plan.

Final Thoughts: Setting Up Dental Clinic Health Insurance

Finding health insurance for your dental team doesn’t have to be like pulling teeth. Whether you choose ICHRA for flexibility or stick with a traditional group plan, the right benefits package will protect your team while improving your power to recruit and retain a great workforce.

If you want to simplify the process, StretchDollar makes ICHRA setup easy—so you can get back to running your practice (and maybe finally enjoy that coffee).