If health insurance and domestic partnerships had a relationship status, it would be “it’s complicated.” While many healthcare plans extend coverage to domestic partners, there are some limitations and differences compared to spouses.

This blog breaks down a lot of the complexities surrounding domestic partnerships and health insurance, but keep in mind that some nuance is needed on this topic.

What Qualifies as a Domestic Partner?

In simple terms, a domestic partner is someone that you share a committed, long-term relationship with. It is similar to marriage in this regard, but without the legal framework.

These are the common criteria used to recognize domestic partnerships:

- Shared residence – You and your partner live together.

- Financial interdependence – Shared financial responsibilities, like joint bank accounts or leases.

- Commitment – Proof of a permanent, exclusive relationship akin to marriage.

Check out the official definition here.

Something that is important to note, domestic partnership benefits (and rights) don’t only vary state-by-state, but also differ county-to-county. Yes, this makes things complicated for everyone. No, it doesn’t make sense.

Can Domestic Partners Be on Each Other’s Health Insurance Plans?

Many employers do provide health insurance options for domestic partners within their group plan. However, they technically won’t be enrolled on the same plan but rather separate plans that receive the provided benefits. For instance, while you both might be receiving the same coverage, you won’t be contributing to a mutual deductible. Like I said…it’s complicated.

It’s important to note that while many employers offer these benefits, not all do as it is not legally required. If you’re unsure whether your partner can be added to your health insurance, reach out to your HR department or review your employer's benefits policy.

If your employer offers an ICHRA, or Individual Coverage Health Reimbursement Arrangement, the rules are slightly different. With an ICHRA, your employer is only choosing a benefit allowance and not the health plan. This allows you to pick a plan that will cover your partner.

(If you want to learn more about the nitty gritty details of an ICHRA, check out this article.)

Marketplace Plans

When shopping on the marketplace there is a little more wiggle room. If you’re in an area that recognizes domestic partnerships AND you pick a plan that allows for it, then it is possible to be on the same plan. However, in the majority of circumstances you’ll face a lot of the same obstacles as a group plan.

Here’s how our health insurance expert Silvia Piscil breaks it down:

“At the federal tax level, the marketplace follows IRS rules, which state that domestic partners are not considered spouses unless they are legally married. This means that domestic partners cannot file jointly unless they are legally married.

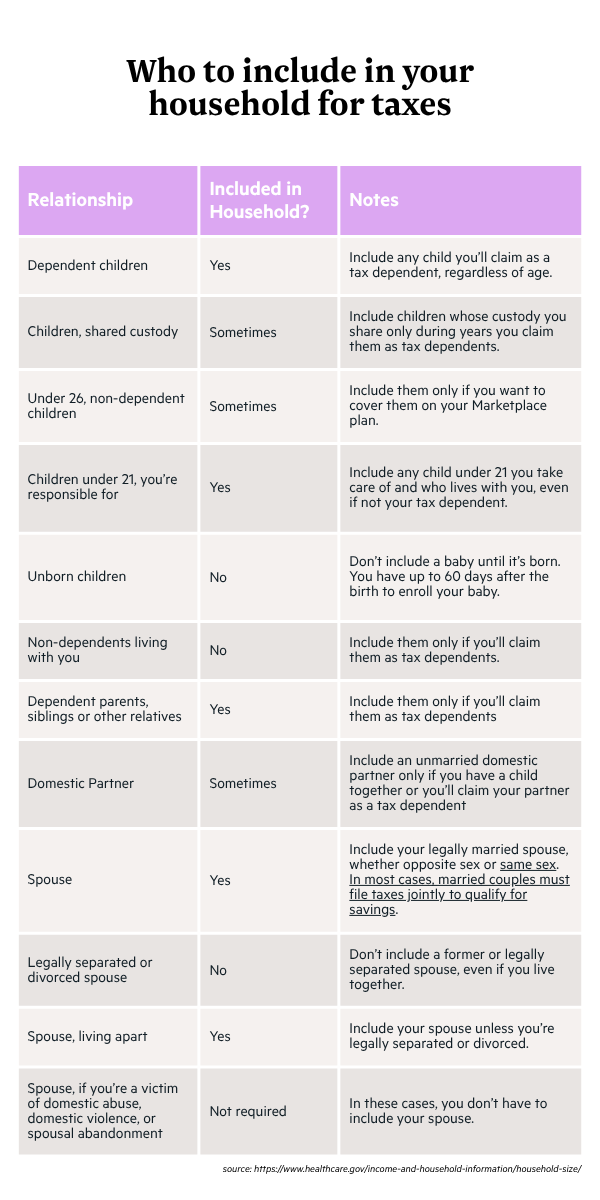

On the flip side, some states have specific rules that require registered domestic partners to split their combined income when determining eligibility for subsidies. You can share a Marketplace plan if one partner qualifies as a tax dependent of the other, or if they share and claim a child who meets IRS dependent criteria.

If one partner decides they do not want to be claimed as a tax dependent, both partners will need to apply for and obtain individual policies.”

Key Differences Between Domestic Partners and Spouses in Health Insurance

While domestic partners may receive similar coverage, there are notable differences to be aware of:

1. Automatic Eligibility

Spouses are automatically eligible for coverage under most health insurance plans upon marriage. Domestic partners, however, must meet and verify specific criteria. Some plans may even outright exclude domestic partners from coverage.

2. Employer Policies

Employers are not legally required to offer health insurance for domestic partners, even in states where domestic partnerships are legally recognized. This contrasts with coverage mandates for spouses under federal laws like the Affordable Care Act.

3. Legal Protections

Under federal law, married couples enjoy more extensive legal benefits, including COBRA continuation rights for health insurance. Domestic partners, on the other hand, are not guaranteed these protections unless specified in their plan.

Tax Implications for Domestic Partners

A major factor to consider when evaluating health insurance for domestic partners is how benefits are taxed. Here’s how it breaks down:

- Tax-Free for Spouses

- Employer contributions to spousal health insurance are typically excluded from taxable income, providing significant savings.

- Imputed Income for Domestic Partners

- Contributions made by an employer to cover domestic partners are considered taxable income for the employee. This is known as “imputed income” and can increase your tax burden significantly.

For example, if your employer covers $5,000 annually to insure your domestic partner, that $5,000 is added to your taxable income. This can raise the amount of taxes you owe, directly affecting your overall financial picture.

Navigating the Tax Implications

- Use tax calculators to estimate how imputed income will affect your tax liability.

- Consider consulting a tax professional for tailored advice.

- Factor in these additional costs when comparing health insurance plans to determine the most cost-effective option.

Although there are some exceptions depending on state and county, there are instances where one can use a partner’s income for the subsidy calculation if you share a tax-household (like sharing a child), but are enrolled separately.

You will want to ensure that all contributions are reported on for the tax year. If a member wishes to add a partner onto a family plan that includes a child, they will need to claim the partner as a dependent.

Denials and Approvals

Here is what Silvia shared regarding her experience:

“A key reason domestic partners are often denied shared benefits is due to the way federal law defines “household” and “family” for tax and insurance purposes. Eligibility for shared coverage and subsidies through the Marketplace is based on federal tax household rules.

For example, in Texas, domestic partners are not recognized under state law. They can’t enroll together in a health plan unless one is claimed as a tax dependent or they share and claim a child as a tax dependent. In one case in Texas, two domestic partners in Dallas shared a home but filed their taxes separately. Because they filed separately, they were required to enroll in two separate policies, and each had to apply for their own plans.

On the other hand, California is more domestic partner-friendly with a state-based marketplace. To qualify, partners must be registered in a domestic partnership that is legally recognized under California state law. California requires all insurers to treat registered domestic partners the same as married couples. In one case I encountered in California, two registered domestic partners lived together and shared expenses. When applying through Covered California, they combined their incomes and enrolled in a single family plan.”

How Domestic Partners Can Shop for Health Benefits

If you and your partner are exploring health insurance options, either with a company traditional group plan or an ICHRA, there are steps you can take to find the best coverage for your unique needs:

Step 1: Understand Your Options

- Find out whether domestic partners are eligible for coverage and what documentation is required for the plan your employer offers or the marketplace plan you choose

- Research state and federal programs that offer individual or family coverage if employer-sponsored insurance isn’t a viable option.

Step 2: Compare Plans

- Evaluate premiums, copays, and deductibles.

- Meet with a broker (aka a licensed health insurance expert) to discuss plans that would meet your needs. They know the nitty gritty of insurance and can help you understand your options.

Step 3: Prepare Documentation

Be ready to provide proof of your domestic partnership. Collect and organize documents such as:

- A domestic partnership affidavit

- Joint financial account statements

- A copy of a lease or mortgage with both partners’ names

- Proof of shared expenses, such as utility bills

Alternative: Explore Individual Plans

If domestic partner coverage isn’t available through an employer, individual plans on the health insurance marketplace could be a better fit. Depending on your household income, you may qualify for subsidies or state-specific programs like Medicaid.

Employers can provide employees with health benefit dollars this way via an ICHRA. If this is something that would benefit you, ask your employer to consider an ICHRA provider for health benefits instead of a traditional small group plan.

Conclusion

#itscomplicated

Knowing what qualifies as a domestic partnership, the differences in coverage, and the tax implications can help domestic partners make informed decisions.

If you’re considering health insurance options for you and your partner, remember to:

- Confirm domestic partner eligibility with your employer.

- Compare plans, taking coverage and tax implications into account.

- Seek guidance from HR professionals, insurance brokers, or tax advisors as needed.

By staying informed and prepared, you can secure a plan that meets your healthcare needs while minimizing financial burdens.