Key takeaways

- Standalone dental and vision plans offer broader provider networks and better coverage than basic health plan add-ons.

- Without insurance, dental and vision care can be surprisingly expensive, but standalone plans are affordable and save you money long-term.

- With StretchDollar and ICHRA, you can use leftover benefit dollars to double dip on dental and vision insurance for maximum coverage.

You’ve probably heard that double dipping is bad manners—but when it comes to insurance, it’s actually a power move. Relying solely on your health plan’s dental and vision add-ons might leave you squinting at price tags and crossing your fingers that your tooth ache is just temporary. Sometimes, taking a second dip into standalone coverage is the smart way to get the protection (and peace of mind) you really want.

Here’s why supplementing your primary health plan with a standalone dental or vision plan is a brilliant strategy to keep your wallet happy and your body healthy.

The Problem with "Good Enough" Coverage

When your health insurance carrier provides dental and vision, it’s often a basic package designed to check a box. This can lead to a few not-so-fun surprises right when you need care the most.

One of the biggest issues? Limited provider networks.

These bundled plans often have a very small, specific list of dentists and optometrists who will accept them. So, that amazing dentist your friend raves about? Or the convenient eye doctor right down the road? There’s a good chance they’re not in your network. You're left with a choice: pay full price out-of-pocket or start a new, awkward relationship with a random provider from a pre-approved list.

It's like having a gift card that's only valid at one store…three towns over…on a Tuesday.

But don’t get me wrong—any coverage is better than no coverage. Your health insurance’s dental/vision add-on is still beneficial and is nothing to stick your nose up at. It is simply a matter of better vs. best.

Can you get dental & vision insurance if your health plan already includes it?

YES! It’s technically called supplemental insurance, but double-dipping has a nicer ring to it. You receive a secondary insurance card when you get that supplemental dental or vision insurance.

So instead of looking at your health insurance carriers website for covered physicians, you can instead look through your dental or vision insurance carriers website of providers.

The Scary Cost of Going Un(der)insured

Let's play a fun game called "Guess the Bill." What do you think a routine root canal costs without any insurance? If you guessed somewhere in the ballpark of a used car, you’re not far off. A root canal can easily run you $1,000 to $2,000 or more. A simple dental crown? That could be another $1,500. A survey by the ADA found that 36% of participants hadn’t been to the dentist in two years, with the number one reason being cost.

Vision care isn't much cheaper. A standard eye exam can cost over $200, and a pair of prescription glasses can set you back $300 to $500, especially if you need progressive lenses or other features. Personally, my needed brand of contact lenses runs around $250 just for a 6 month supply. Suddenly, that "free" vision rider on your health plan that only covers $100 for frames seems a lot less generous.

The Surprisingly Affordable Solution

Here's the good news. Standalone dental and vision plans are more affordable than you might expect. While health insurance can cost hundreds (or thousands) per month, you can often find a solid dental plan for just $20 to $50 a month. A good vision plan might only cost you $10 to $20 a month.

I am aware that saying “just” might sound obtuse, especially in today’s economy. We are playing the game of comparison here. That $1,500 root canal + $1,500 crown is a lot more daunting than “just” $30 a month.

For the price of a few fancy coffees, you get access to a wider network of doctors, better coverage for major procedures, and higher allowances for things like glasses and contacts. It’s a small(er) monthly cost that can save you from a massive, unexpected bill down the road. You’re not just buying insurance; you’re buying peace of mind and the freedom to choose your own provider.

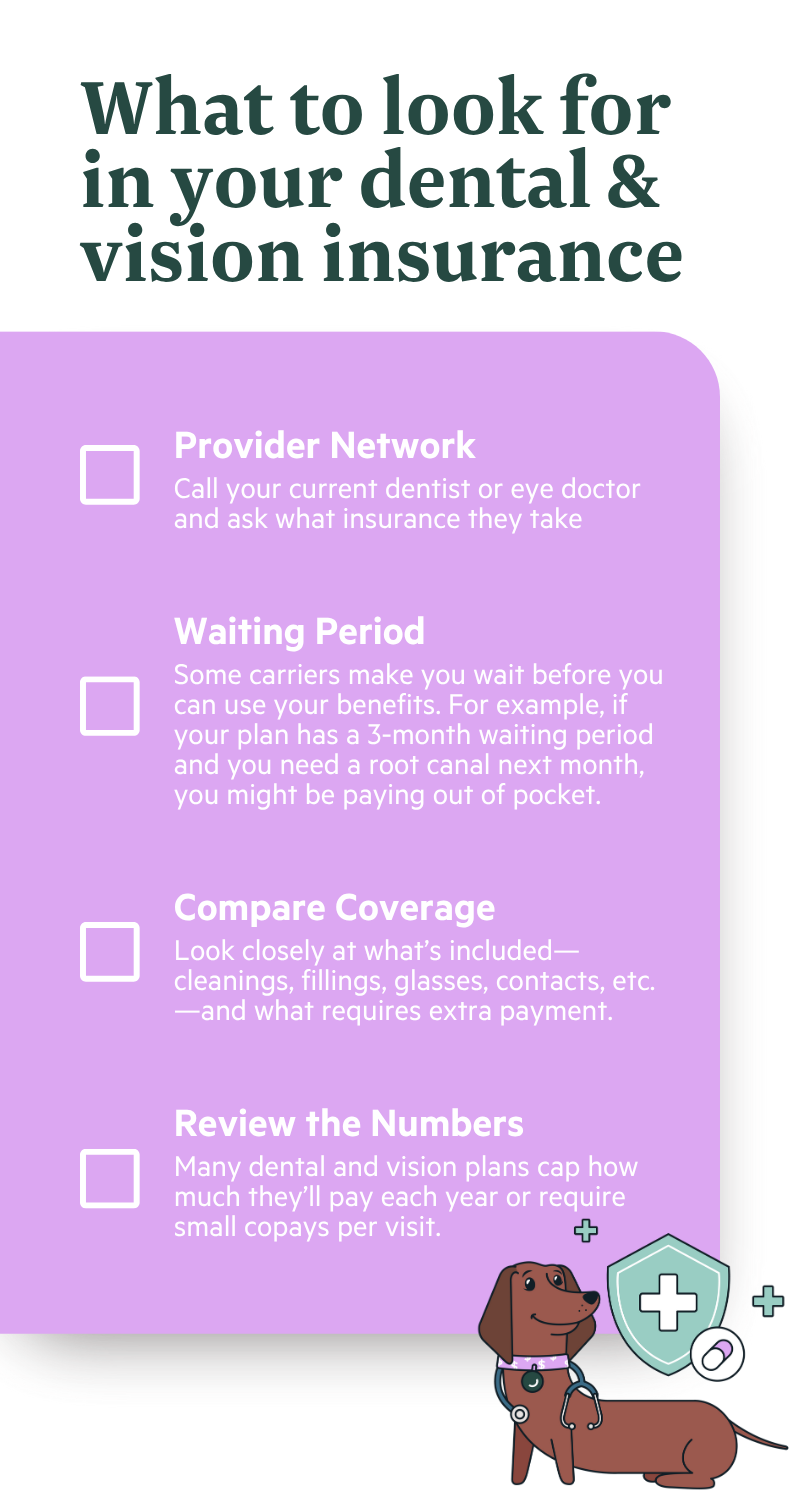

What Should You Look for (in Your Vision & Dental Plan)?

Not all vision and dental plans are alike (just like health plans!) How do you find one right for you?

Here’s a quick list:

- Check the provider network.

- If you already have a favorite dentist or eye doctor, call their office and ask which insurance plans they accept.

- Understand the waiting period.

- Some carriers make you wait before you can use your benefits. Sometimes that’s true for all services, sometimes it's just for major ones. For example, if your plan has a 3-month waiting period and you need a root canal next month, you might be paying out of pocket.

- Compare coverage details.

- Look closely at what’s included—cleanings, fillings, glasses, contacts, etc.—and what requires extra payment.

- Review annual limits and copays.

- Many dental and vision plans cap how much they’ll pay each year or require small copays per visit.

A Better Way to Pay with ICHRA

If you get your health benefits through an ICHRA (Individual Coverage Health Reimbursement Arrangement) with a provider like StretchDollar, you’re sitting in an even better position. ICHRA gives you a set amount of tax-free money from your employer each month to buy health coverage. Not sure what an ICHRA is? Dig deeper right here: A Not-So-Boring, One-Page Guide to ICHRA.

Here's the kicker: as long as you purchase a qualifying health plan, you can use any leftover allowance on other medical expenses, including standalone dental and vision insurance premiums.

This means you can pick a great health plan and double dip on robust dental and vision coverage, all while using your tax-free benefit dollars. It’s your money, and you get to decide how to best protect your health from head to toe.

So go ahead, be a double dipper. Your teeth, your eyes, and your bank account will thank you.