Let’s just say this year’s open enrollment didn’t exactly roll out the red carpet. Normally, we’re able to analyze ACA pricing weeks—sometimes even months—in advance. But for 2026, premium data dropped just a few days before the November 1st kickoff. If you pictured analysts scrambling over a weekend to crunch numbers, you’re not far off. The good news? Instead of leaving you to dig through mountains of spreadsheets, we did the heavy lifting and pulled together the key details—so you don’t have to.

For 2026, things are getting even more interesting. While the headline number is an 11% average premium increase nationally, that figure is a bit of a mirage. The real story is hiding in the details.

Depending on where your employees live, their premium change could be a rounding error or a gut punch. This analysis will break down what’s happening, where the best deals are, and how you can help your team shop smarter for a plan that works for them without breaking your budget.

We went through and analyzed the 138 most populated major metros in the US looking at the lowest cost bronze, gold, silver, and $0 deductible plans (or as close as we can get). Here’s some of what we found out to expect in 2026:

Location, Location, Location: Premium Hikes Vary Wildly

The national average premium increase masks enormous regional differences. An employee's zip code is now the single biggest factor determining what they'll pay for health insurance in 2026. Geography matters more than ever.

Some cities are facing sticker shock that will make your eyes water.

- Providence, RI: Brace yourself. Bronze plan premiums here shot up 28%, from $266 to $340 per month. Gold plans weren't far behind, with a 41.0% jump from $369 to $521.

- Wichita, KS: Residents here are feeling similar pain, with Gold plans leaping 68.3%, from an average of $451 to a hefty $759 per month.

Meanwhile, in several major metro areas, the story is completely different. Many are seeing manageable increases or even decreases.

- Los Angeles, CA: Bronze +2.9%, Gold -1.1% (Yes, a decrease!)

- San Francisco, CA: Bronze +0.8%, Gold +1.6%

- Boston, MA: Bronze -1.2%, Gold +10.1%

- San Jose, CA: Bronze +0.8%, Gold +2.1%

- San Diego, CA: Bronze +4.6%, Gold +7.2%

- Washington D.C.: Bronze +4.8%, Gold +6.8%

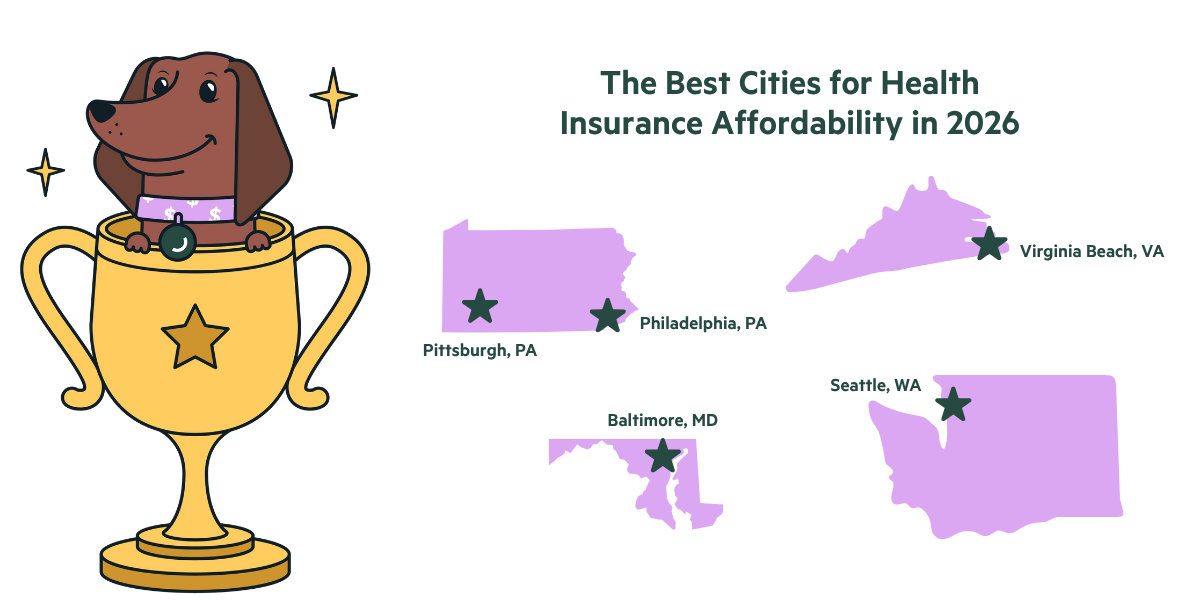

The Best Cities for Health Insurance Affordability in 2026

When you look beyond just the monthly premium and factor in deductibles and copays, a clear list of value winners emerges. These cities offer the best bang for your buck.

Top 5 Overall Value Cities:

- Pittsburgh, PA: Boasts the #1 lowest Gold premium nationally at just $353/month, paired with excellent specialist copays.

- Baltimore, MD: A very close second, with the #2 Gold premium at $359/month and a competitive deductible.

- Philadelphia, PA: Offers a low $424/month premium combined with an ultra-low $800 deductible for Gold plans.

- Virginia Beach, VA: A strong contender with a $432/month premium and elite-level copays for both primary and specialist visits.

- Seattle, WA: Combines a low $424/month premium with top-tier specialist copays.

A note on Baltimore vs. Pittsburgh: While Baltimore has the absolute lowest Bronze premium in the country ($272/mo) and the second-lowest Gold premium, Pittsburgh clinches the top spot due to a slightly better overall copay structure. Both are exceptional choices.

Major Metro Winners:

- Los Angeles: Unbeatable for anyone expecting to use their healthcare, offering the #1 deductible in the nation: $0.

- Chicago: Home to the single best specialist copay in the country—just $10 on some plans.

- Houston: A great balance of a top-20 deductible ($500) and elite specialist copays.

The Smart Shopper's Secret: Why Gold Beats Bronze

Does picking the plan with the lowest monthly premium really save money? Not usually. The "cheapest" Bronze plans often come with terrifyingly high deductibles, sometimes between $8,500 and $10,600. That means your employees pay for everything out-of-pocket until they hit that massive number.

Here’s the secret: upgrading to a Gold plan with day-one coverage is often cheaper than you’d think. The monthly premium difference can be as little as $40-$80.

- In Pittsburgh, it's just a $55/month difference to go from a high-deductible Bronze plan to a Gold plan.

- In Albuquerque, it’s only $44/month more for immediate access to care.

- In Chicago, an extra $81/month gets access to that incredible $10 specialist copay instead of no coverage until the deductible is met.

For anyone who plans to see a doctor even once or twice, the math is clear. Paying a little more per month for a Gold plan can save thousands in out-of-pocket costs. Our analysis also shows that if you compare plans with similar day-one access, the true year-over-year premium increase is closer to 15%, not the scary 18.8% average.

The Silver Lining of "Silver Loading"

A market quirk called "silver loading" is creating a golden opportunity for savvy shoppers in 2026. Because subsidies are tied to Silver plan prices, those premiums are often artificially inflated.

The result? In many areas, Gold plans—which have better benefits like lower deductibles and copays—are now priced similarly to or even cheaper than Silver plans. We're seeing Gold plans priced within $10-$30 of Silver plans.

The Strategy: If your employees do not qualify for subsidies (Cost-Sharing Reductions), they should almost certainly skip Silver plans entirely. Compare the cheapest Bronze plans against the best-value Gold plans to see what makes sense for their health and budget.

A Word of Caution for the 60-64 Age Group

Unfortunately, premium increases are not distributed evenly across age groups. Those aged 60-64 are being hit the hardest, with many seeing increases 25-35% higher than the national average. If you have key team members in this bracket, it's critical to budget for this and ensure they lock in 2026 rates before Open Enrollment ends.

Carrier Trends: Brand Loyalty is Expensive

Thinking of sticking with a familiar insurance carrier? You might want to reconsider.

- Blue Cross/Blue Shield regional plans are showing hikes of 20-30%.

- UnitedHealthcare is also implementing significant premium increases.

- Meanwhile, regional carriers like Ambetter, Oscar, Molina, and Kaiser are often offering premiums 10-20% lower than the legacy giants.

The lesson is simple: shop across all available carriers. Sticking with a familiar name could cost your employees hundreds of dollars every month.

Why This Matters for You—and Your Small Business

If you’re considering an Individual Coverage Health Reimbursement Arrangement (ICHRA)—whether you’re an employee weighing options or a business owner planning your next move—the 2026 rate landscape should grab your attention. With an ICHRA, you reimburse workers for individual market premiums instead of locking into a traditional group plan. Suddenly, all these ACA price swings and regional quirks matter a lot more to your bottom line.

Here’s the twist: while the ACA individual market used to be seen as unpredictable and pricey, recent years have brought major stabilization. In fact, ACA premiums in many regions now closely mirror employer-sponsored plan costs, according to BenefitsPRO1. For 2026, both markets are bracing for increases, but the gap is narrower than ever—and in some cities, ACA plans can offer better value.

Meanwhile, small businesses are facing their own set of challenges. The average small group health plan is projected to jump 11% this year, according to KFF analysis2. As a business owner, you already know that double-digit premium hikes can stretch budgets to the breaking point—or push you to drop coverage altogether.

This is where the flexibility of ICHRAs shines. Instead of fighting rising group plan costs, you can set a defined benefit and let employees shop the individual market—often with more plan options and the potential to “upgrade” to a Gold plan for a modest cost. For your business, this means better benefits control, and for your team, it could open the door to plans that work smarter for their needs.

Bottom line? Don’t assume the status quo is your best bet.

The only way to be sure you’re getting your money’s worth is to compare individual market plans with small-group offerings in your area. With ACA premiums now tracking closely with employer coverage, smart comparison-shopping is the best prescription for cost-effectiveness and peace of mind. For some, an ICHRA-funded ACA plan could provide better options and cost control than the small-group market. But with so many price swings, it’s vital to take a closer look before deciding.

Should You Shop On or Off the Exchange?

For 2026, more insurers are offering plans "off-exchange," meaning directly through their websites or brokers. While these plans are not eligible for subsidies, they can sometimes feature smaller premium increases.

If you know your employees don't qualify for subsidies, it's worth exploring these off-exchange options—they might uncover a better deal. Need help figuring out which is best for your team? Check out this in-depth guide to on-exchange vs. off-exchange health insurance for the pros, cons, and a few tips to make the choice easier.

The Blurring Lines of Plan Types (HMO vs. EPO vs. PPO)

The alphabet soup of plan types is getting murkier. We're seeing identical plans filed as an "HMO" in one state and an "EPO" in another. "Open Panel HMOs" function just like EPOs, and "Closed Network PPOs" are essentially EPOs in disguise. True PPOs are becoming a rare breed. You can break down the acronmyn soup here.

Don't get hung up on the label. Instead, investigate the details:

- How big is the provider network?

- Does an employee need a referral to see a specialist?

- Is there any coverage for out-of-network care?

Your 2026 ACA Shopping Checklist

To find the best plan for your team, focus on what matters most. Here’s a checklist to guide you through Open Enrollment:

- Assess Your Team's Needs: Honestly evaluate how often your employees might see a doctor, fill prescriptions, or need specialist care.

- Compare Bronze vs. Gold: Don't just look at the premium. Calculate the cost for an employee to upgrade from a high-deductible Bronze plan to a Gold plan with day-one copays.

- Verify Your Network: Make sure your team's preferred doctors, specialists, and hospitals are in-network before you commit.

- Model Total Costs: Add up monthly premiums plus potential deductibles and copays based on expected usage to estimate the total annual cost of care.

- Check for Subsidies: If an employee's income qualifies, a Silver plan might still be their best option due to powerful Cost-Sharing Reductions.

- Explore Off-Exchange: If your employees don't qualify for subsidies, look at plans sold directly by carriers.

- Shop All Carriers: Forget brand loyalty. Compare every single option available in your area.

Confirm Prescriptions: Double-check that essential medications are covered under the plan's drug formulary.

Sources:

KFF: How Much and Why Premiums are Going up for Small Businesses in 2026

BenefitsPRO: ACA premiums stabilize, nearly mirroring employer-sponsored coverage costs