Key takeaways

- ACA plans cover emergency care anywhere in the U.S., but routine or non-emergency care may only be covered within your network.

- Consider PPO or EPO plans for greater flexibility with out-of-network care, which can benefit frequent travelers needing coverage in different locations.

Many people love to travel, but your health insurance plan might be more of a homebody. Marketplace plans offer crucial protections, but travelers face unique challenges. This article explores how ACA coverage works when you’re on the move, what to look out for, and how to choose a plan that fits your lifestyle.

The Core Challenge: Your Plan's Home Turf

The main thing to understand about ACA plans is that they are generally tied to a specific state and a local network of doctors and hospitals. Think of your plan as having a "home base." While it will cover true emergency care anywhere in the U.S., routine care—like a check-up, a visit to a specialist, or a planned procedure—is a different story. For that, you typically need to be in your “home base” and use providers within your plan’s network.

This is where travelers can get into trouble. You might have a top-tier plan at home, but if you're three states away and need to see a doctor for a non-emergency issue, you could be facing a hefty out-of-pocket bill.

(This is also why if you move to another state or even county, you need to let your health insurance know! Moving is a qualifying life event so you’ll also get the chance to shop for a new health plan.)

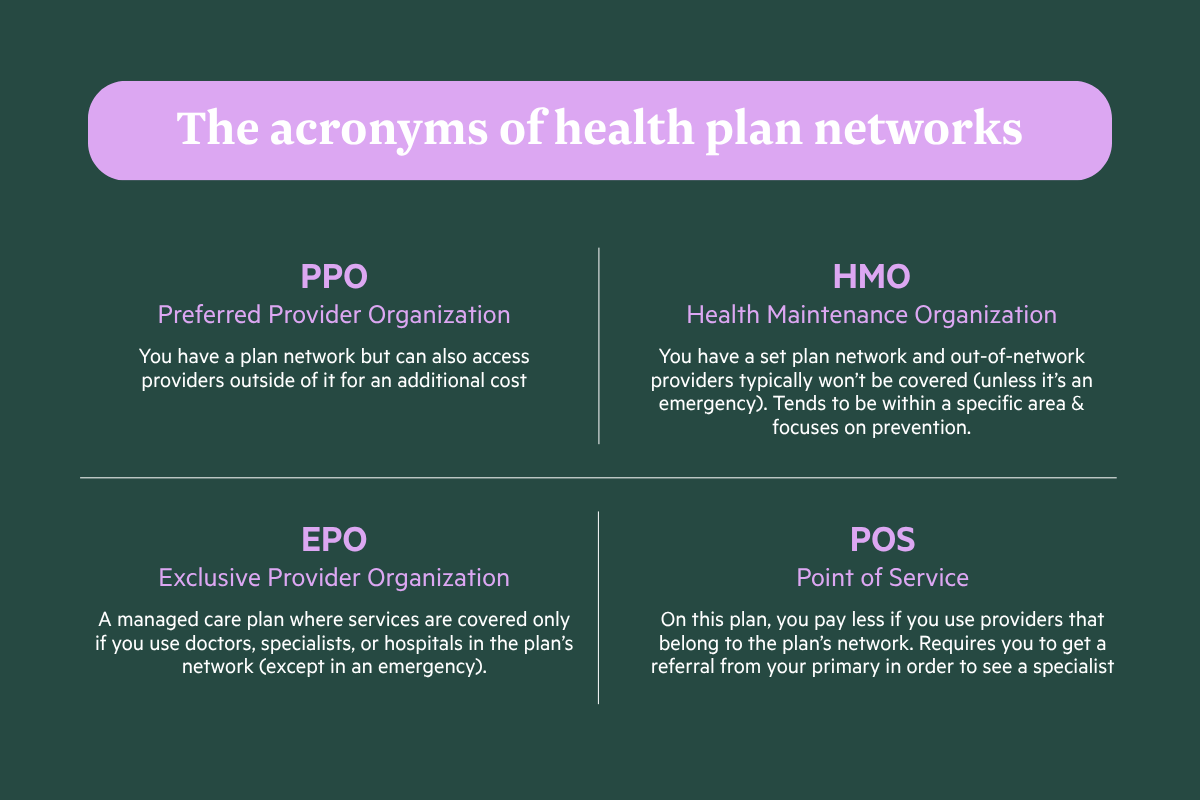

Network Restrictions: The Alphabet Soup of Coverage (HMO, EPO, PPO)

The biggest hurdle for travelers is network restrictions. The type of plan you have dictates your freedom to get care outside your local area.

- HMO (Health Maintenance Organization): This type of health plan has the narrowest network – choices are more limited and as such you pay less for premiums. These plans are not the best choice for travelers.

- EPO (Exclusive Provider Organization): These plans are often more affordable but come with the tightest geographic restrictions. They require you to use a specific network of doctors and hospitals. If you get care outside that network, it's generally not covered unless it's a life-or-limb emergency. For a traveler, this means routine care is off the table until you get back home.

- PPO (Preferred Provider Organization): These plans are the traveler's best friend. PPOs offer more flexibility to see out-of-network providers, though you'll usually pay more for it. Many PPOs have a nationwide network, making it easier to find covered care when you're traveling. However, not every state offers PPOs on the Marketplace, and they tend to have dramatically higher monthly premiums.

You can learn more about the alphabet soup definitions here.

Real-Life Scenarios

Let's see how this plays out in the real world:

Example 1: Alex, the Freelance Photographer

Alex is a photographer who lives in Texas but spends months on the road for assignments. He has an HMO plan because the premium was low. While on a shoot in Colorado, he develops a persistent sinus infection. He finds a local urgent care clinic, but because it's out-of-network and not a life-threatening emergency, his insurance denies the claim. Alex is stuck paying the full $300 bill himself.

Example 2: The Garcia Family's Cross-Country Road Trip

The Garcias are taking their two kids on a summer road trip from Florida to California. They have a PPO plan. Midway through their trip in Arizona, their youngest, Leo, takes a tumble at the Grand Canyon and needs stitches. They head to a nearby emergency room. Because it’s an emergency, their ACA plan is required to cover it. Later, when Leo needs his stitches removed in Utah, they use their PPO's nationwide directory to find an in-network urgent care clinic, and the visit is covered just as it would have been at home.

What Counts as an "Emergency"?

This is a critical distinction. The ACA mandates that all Marketplace plans cover emergency care at out-of-network hospitals. Let’s repeat that one. All Marketplace plans cover emergency care at out-of-network hospitals. The idea that they don’t is a common misconception about ACA plans.

However, the definition of an "emergency" is key. According to healthcare experts, it's not just about what you think is an emergency, but what a "prudent layperson" would consider a situation that could cause serious jeopardy to your health.

As the Kaiser Family Foundation notes, plans can't charge you more for out-of-network emergency services than they would for in-network ones. But the catch is what happens after you're stabilized. Any follow-up care could be considered non-emergency and may not be covered if you're still out-of-network.

Tips for Choosing the Right Plan for Your Travels

If you know you’ll be on the move, here’s how to pick a plan that won’t leave you stranded:

1. Prioritize a PPO if Possible: If your state's Marketplace offers PPOs and you can fit the higher premium into your budget, it's usually the best choice for frequent travelers. If not possible, choose an EPO (larger network than HMO) and contact the carrier to learn about the in-network urgent care before you travel.

2. Establish a Home Base: You need a permanent address in one state to apply for an ACA plan. Even if you’re a full-time RVer, you must declare a state of residence. This is the state where you’ll enroll and where your primary network will be.

3. Investigate Nationwide Networks: Before enrolling in a PPO, check which insurance carriers have robust nationwide networks. Some are much better than others. Call the insurer and ask directly about coverage in the states you visit most often.

4. Embrace Telehealth: Many plans now offer telehealth services, allowing you to have a virtual visit with a doctor for minor issues. This can be a great way to get prescriptions or medical advice from an in-network provider, no matter where you are.

5. Plan Your Routine Care: If you know you'll be back in your home state in a few months, schedule your annual physicals, dental cleanings, and non-urgent specialist visits for that time. A little planning can save you a lot of money.

Travel with Confidence

Having an ACA plan doesn't mean you have to stay home. It just means you need to be a little smarter about your coverage. By understanding your plan’s network, knowing the difference between emergency and routine care, and choosing the right plan type from the start, you can have both the freedom of travel and the peace of mind that comes with solid health insurance.